Saturday, June 27, 2009

The SEC Needs Your Feedback

http://zerohedge.blogspot.com/2009/06/sec-needs-your-feedback.html#disqus_thread

Banks SIezed by FDIC: 45 to Date 2009

FDIC Link here

On Friday, June 26, 2009, Mirae Bank, Los Angeles, CA was closed by the California Department of Financial Institutions, and the Federal Deposit Insurance Corporation (FDIC) was named Receiver. No advance notice is given to the public when a financial institution is closed. The FDIC has assembled useful information regarding your relationship with this institution. Besides a checking account, you may have Certificates of Deposit, a car loan, a business checking account, a commercial loan, a Social Security direct deposit, and other relationships with the institution. The FDIC

On Friday, June 26, 2009, Mirae Bank, Los Angeles, CA was closed by the California Department of Financial Institutions, and the Federal Deposit Insurance Corporation (FDIC) was named Receiver. No advance notice is given to the public when a financial institution is closed. The FDIC has assembled useful information regarding your relationship with this institution. Besides a checking account, you may have Certificates of Deposit, a car loan, a business checking account, a commercial loan, a Social Security direct deposit, and other relationships with the institution. The FDIC

| Failed Bank List | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Friday, June 26, 2009

Overseas markets clearly will offer the greatest returns in the months and years to come, BUT federal regulations prohibit most American investors

Money Morning Sign Up Confirmation - Dollar Report

If you give us a few minutes a day, we’ll show you how to profit from the global boom of a lifetime…

Dear Reader:

Welcome to Money Morning.

And congratulations.

By signing up for our new free daily e-letter, you’ve just made a made one of the shrewdest moves possible toward a successful financial future.

Your free research report, Why the Federal Reserve Can’t

Save the Dollar… Is available here - http://www.moneymorning.com/report/Dollar_Report_MMDOL08082.pdf

And that’s just for starters.

Each and every weekday, Money Morning will tell you about the top investment opportunities from all around the world.

It will be delivered straight to your e-mail inbox.

And it won’t cost you a cent.

Believe me when I say that say that your timing was perfect.

You see, we’re in the early stages of an unprecedented global boom - bigger, longer lasting and with a greater number of impossible-to-predict ramifications than any we’ll see again.

From 2005 to 2010 alone, the value of all the stocks, bonds, CDs and other financial assets held worldwide will soar from $118 trillion to $200 trillion, the highly respected McKinsey Global Institute reported in a just-released report.

That’s an increase of $82 trillion, or 69%. In just five years.

The boom will certainly redistribute wealth. But it will also radically alter the global economic pecking order. And in a big way.

Right now, Asia and the United States each account for 28% of the world economy. The World Bank estimates that America’s share of the world economy will slip a bit, dropping to 24% by 2030.

But Asia’s share will double, reaching a staggering 55%.

In other words, the Asia of tomorrow will be twice as powerful as the United States of today.

Retail investors who ignore these powerful trends and adhere to U.S.-only portfolios will ultimately realize that they’ve been left behind financially.

Wharton Professor and best-selling author Jeremy Siegel recently said investors should toss away the old international-investing allocation of 5% to 15%. Even the average investor should have 40% of their holdings in overseas investments, he said.

Unfortunately, that’s not going to be as easy as it sounds. And you’ll be surprised at the two reasons why.

Sad Fact #1: While the average American doesn’t have access to the "market intelligence" needed to profit from this overseas boom, the nation’s well-connected wealthy investors are taking these projections straight to the bank - and are already profiting from some of the very best deals. Wall Street has known about this global boom for some time. But they’re reserving their best profit opportunities for their wealthiest clients.

Even investors who see and understand what’s happening could end up watching this wealth explosion from the wrong side of the velvet rope. That’s because …

Sad Fact #2: Even though overseas markets clearly will offer the greatest returns in the months and years to come, federal regulations prohibit most American investors from buying many foreign stocks.

You heard that correctly.

If a foreign company isn’t registered with the Securities and Exchange Commission, its shares are off-limits to most investors. And the shortage of foreign shares is getting worse, instead of better: The labyrinthine-and-costly registration process is even discouraging foreign companies from listing easy-to-trade American Depository Receipts (ADRs), a type of security U.S. investors trust and are willing to buy.

Wealthy investors don’t face this problem. An obscure SEC regulation, Rule 144A, allows them to circumnavigate that rule and form investment pools through investment banks, so they can buy foreign-company shares.

But if you’re not yet fortunate enough to be a millionaire investor, aren’t a partner at Merrill Lynch, or don’t live next door to the CEO of Goldman Sachs, the game isn’t over for you.

Money Morning can show you the way.

In addition to daily news, analysis and recommendations, you’ll also get free access to our Money Morning archives, containing investment research, educational reports and special profit opportunities.

Just log on to: www.moneymorning.com. It’s free.

Your Money Morning dispatches will begin arriving via e-mail in two or three days. In the meantime, look for your free bonus research report, The 3 Best Investments in Asia Today, to arrive in your inbox.

Again, welcome aboard. And congratulations on taking advantage of what could be the biggest financial boom since the Industrial Revolution. You’ll be glad that you did.

Good investing,

William Patalon III

Managing Editor

Money Morning

P.S. Right now, an additional $867 billion is about to flow into critical new markets such as Asia and Latin America. Eight companies in particular are poised to leapfrog such blue chip rivals as Boeing, Novartis, GE and Black and Decker. To see more about these fast-moving profit generators, click hereDe-Dollarization: Dismantling America’s Financial-Military Empire The Yekaterinburg Turning Point by Prof. Michael Hudson

The city of Yakaterinburg, Russia’s largest east of the Urals, may become known not only as the death place of the tsars but of American hegemony too – and not only where US U-2 pilot Gary Powers was shot down in 1960, but where the US-centered international financial order was brought to ground.

Challenging America will be the prime focus of extended meetings in Yekaterinburg, Russia (formerly Sverdlovsk) today and tomorrow (June 15-16) for Chinese President Hu Jintao, Russian President Dmitry Medvedev and other top officials of the six-nation Shanghai Cooperation Organization (SCO). The alliance is comprised of Russia, China, Kazakhstan, Tajikistan, Kyrghyzstan and Uzbekistan, with observer status for Iran, India, Pakistan and Mongolia. It will be joined on Tuesday by Brazil for trade discussions among the BRIC nations (Brazil, Russia, India and China).

The attendees have assured American diplomats that dismantling the US financial and military empire is not their aim. They simply want to discuss mutual aid – but in a way that has no role for the United States, NATO or the US dollar as a vehicle for trade. US diplomats may well ask what this really means, if not a move to make US hegemony obsolete. That is what a multipolar world means, after all. For starters, in 2005 the SCO asked Washington to set a timeline to withdraw from its military bases in Central Asia. Two years later the SCO countries formally aligned themselves with the former CIS republics belonging to the Collective Security Treaty Organization (CSTO), established in 2002 as a counterweight to NATO.

Yet the meeting has elicited only a collective yawn from the US and even European press despite its agenda is to replace the global dollar standard with a new financial and military defense system. A Council on Foreign Relations spokesman has said he hardly can imagine that Russia and China can overcome their geopolitical rivalry,1 suggesting that America can use the divide-and-conquer that Britain used so deftly for many centuries in fragmenting foreign opposition to its own empire. But George W. Bush (“I’m a uniter, not a divider”) built on the Clinton administration’s legacy in driving Russia, China and their neighbors to find a common ground when it comes to finding an alternative to the dollar and hence to the US ability to run balance-of-payments deficits ad infinitum.

What may prove to be the last rites of American hegemony began already in April at the G-20 conference, and became even more explicit at the St. Petersburg International Economic Forum on June 5, when Mr. Medvedev called for China, Russia and India to “build an increasingly multipolar world order.” What this means in plain English is: We have reached our limit in subsidizing the United States’ military encirclement of Eurasia while also allowing the US to appropriate our exports, companies, stocks and real estate in exchange for paper money of questionable worth.

"The artificially maintained unipolar system,” Mr. Medvedev spelled out, is based on “one big centre of consumption, financed by a growing deficit, and thus growing debts, one formerly strong reserve currency, and one dominant system of assessing assets and risks.”2 At the root of the global financial crisis, he concluded, is that the United States makes too little and spends too much. Especially upsetting is its military spending, such as the stepped-up US military aid to Georgia announced just last week, the NATO missile shield in Eastern Europe and the US buildup in the oil-rich Middle East and Central Asia.

The sticking point with all these countries is the US ability to print unlimited amounts of dollars. Overspending by US consumers on imports in excess of exports, US buy-outs of foreign companies and real estate, and the dollars that the Pentagon spends abroad all end up in foreign central banks. These agencies then face a hard choice: either to recycle these dollars back to the United States by purchasing US Treasury bills, or to let the “free market” force up their currency relative to the dollar – thereby pricing their exports out of world markets and hence creating domestic unemployment and business insolvency.

When China and other countries recycle their dollar inflows by buying US Treasury bills to “invest” in the United States, this buildup is not really voluntary. It does not reflect faith in the U.S. economy enriching foreign central banks for their savings, or any calculated investment preference, but simply a lack of alternatives. “Free markets” US-style hook countries into a system that forces them to accept dollars without limit. Now they want out.

This means creating a new alternative. Rather than making merely “cosmetic changes as some countries and perhaps the international financial organisations themselves might want,” Mr. Medvedev ended his St. Petersburg speech, “what we need are financial institutions of a completely new type, where particular political issues and motives, and particular countries will not dominate.”

When foreign military spending forced the US balance of payments into deficit and drove the United States off gold in 1971, central banks were left without the traditional asset used to settle payments imbalances. The alternative by default was to invest their subsequent payments inflows in US Treasury bonds, as if these still were “as good as gold.” Central banks now hold $4 trillion of these bonds in their international reserves – land these loans have financed most of the US Government’s domestic budget deficits for over three decades now! Given the fact that about half of US Government discretionary spending is for military operations – including more than 750 foreign military bases and increasingly expensive operations in the oil-producing and transporting countries – the international financial system is organized in a way that finances the Pentagon, along with US buyouts of foreign assets expected to yield much more than the Treasury bonds that foreign central banks hold.

The main political issue confronting the world’s central banks is therefore how to avoid adding yet more dollars to their reserves and thereby financing yet further US deficit spending – including military spending on their borders?

For starters, the six SCO countries and BRIC countries intend to trade in their own currencies so as to get the benefit of mutual credit that the United States until now has monopolized for itself. Toward this end, China has struck bilateral deals with Argentina and Brazil to denominate their trade in renminbi rather than the dollar, sterling or euros,3 and two weeks ago China reached an agreement with Malaysia to denominate trade between the two countries in renminbi.[4] Former Prime Minister Tun Dr. Mahathir Mohamad explained to me in January that as a Muslim country, Malaysia wants to avoid doing anything that would facilitate US military action against Islamic countries, including Palestine. The nation has too many dollar assets as it is, his colleagues explained. Central bank governor Zhou Xiaochuan of the People's Bank of China wrote an official statement on its website that the goal is now to create a reserve currency “that is disconnected from individual nations.”5 This is the aim of the discussions in Yekaterinburg.

In addition to avoiding financing the US buyout of their own industry and the US military encirclement of the globe, China, Russia and other countries no doubt would like to get the same kind of free ride that America has been getting. As matters stand, they see the United States as a lawless nation, financially as well as militarily. How else to characterize a nation that holds out a set of laws for others – on war, debt repayment and treatment of prisoners – but ignores them itself? The United States is now the world’s largest debtor yet has avoided the pain of “structural adjustments” imposed on other debtor economies. US interest-rate and tax reductions in the face of exploding trade and budget deficits are seen as the height of hypocrisy in view of the austerity programs that Washington forces on other countries via the IMF and other Washington vehicles.

The United States tells debtor economies to sell off their public utilities and natural resources, raise their interest rates and increase taxes while gutting their social safety nets to squeeze out money to pay creditors. And at home, Congress blocked China’s CNOOK from buying Unocal on grounds of national security, much as it blocked Dubai from buying US ports and other sovereign wealth funds from buying into key infrastructure. Foreigners are invited to emulate the Japanese purchase of white elephant trophies such as Rockefeller Center, on which investors quickly lost a billion dollars and ended up walking away.

In this respect the US has not really given China and other payments-surplus nations much alternative but to find a way to avoid further dollar buildups. To date, China’s attempts to diversify its dollar holdings beyond Treasury bonds have not proved very successful. For starters, Hank Paulson of Goldman Sachs steered its central bank into higher-yielding Fannie Mae and Freddie Mac securities, explaining that these were de facto public obligations. They collapsed in 2008, but at least the US Government took these two mortgage-lending agencies over, formally adding their $5.2 trillion in obligations onto the national debt. In fact, it was largely foreign official investment that prompted the bailout. Imposing a loss for foreign official agencies would have broken the Treasury-bill standard then and there, not only by utterly destroying US credibility but because there simply are too few Government bonds to absorb the dollars being flooded into the world economy by the soaring US balance-of-payments deficits.

Seeking more of an equity position to protect the value of their dollar holdings as the Federal Reserve’s credit bubble drove interest rates down China’s sovereign wealth funds sought to diversify in late 2007. China bought stakes in the well-connected Blackstone equity fund and Morgan Stanley on Wall Street, Barclays in Britain South Africa’s Standard Bank (once affiliated with Chase Manhattan back in the apartheid 1960s) and in the soon-to-collapse Belgian financial conglomerate Fortis. But the US financial sector was collapsing under the weight of its debt pyramiding, and prices for shares plunged for banks and investment firms across the globe.

Foreigners see the IMF, World Bank and World Trade Organization as Washington surrogates in a financial system backed by American military bases and aircraft carriers encircling the globe. But this military domination is a vestige of an American empire no longer able to rule by economic strength. US military power is muscle-bound, based more on atomic weaponry and long-distance air strikes than on ground operations, which have become too politically unpopular to mount on any large scale.

On the economic front there is no foreseeable way in which the United States can work off the $4 trillion it owes foreign governments, their central banks and the sovereign wealth funds set up to dispose of the global dollar glut. America has become a deadbeat – and indeed, a militarily aggressive one as it seeks to hold onto the unique power it once earned by economic means. The problem is how to constrain its behavior. Yu Yongding, a former Chinese central bank advisor now with China’s Academy of Sciences, suggested that US Treasury Secretary Tim Geithner be advised that the United States should “save” first and foremost by cutting back its military budget. “U.S. tax revenue is not likely to increase in the short term because of low economic growth, inflexible expenditures and the cost of ‘fighting two wars.’”6

At present it is foreign savings, not those of Americans that are financing the US budget deficit by buying most Treasury bonds. The effect is taxation without representation for foreign voters as to how the US Government uses their forced savings. It therefore is necessary for financial diplomats to broaden the scope of their policy-making beyond the private-sector marketplace. Exchange rates are determined by many factors besides “consumers wielding credit cards,” the usual euphemism that the US media cite for America’s balance-of-payments deficit. Since the 13th century, war has been a dominating factor in the balance of payments of leading nations – and of their national debts. Government bond financing consists mainly of war debts, as normal peacetime budgets tend to be balanced. This links the war budget directly to the balance of payments and exchange rates.

Foreign nations see themselves stuck with unpayable IOUs – under conditions where, if they move to stop the US free lunch, the dollar will plunge and their dollar holdings will fall in value relative to their own domestic currencies and other currencies. If China’s currency rises by 10% against the dollar, its central bank will show the equivalent of a $200 million loss on its $2 trillion of dollar holdings as denominated in yuan. This explains why, when bond ratings agencies talk of the US Treasury securities losing their AAA rating, they don’t mean that the government cannot simply print the paper dollars to “make good” on these bonds. They mean that dollars will depreciate in international value. And that is just what is now occurring. When Mr. Geithner put on his serious face and told an audience at Peking University in early June that he believed in a “strong dollar” and China’s US investments therefore were safe and sound, he was greeted with derisive laughter.7

Anticipation of a rise in China’s exchange rate provides an incentive for speculators to seek to borrow in dollars to buy renminbi and benefit from the appreciation. For China, the problem is that this speculative inflow would become a self-fulfilling prophecy by forcing up its currency. So the problem of international reserves is inherently linked to that of capital controls. Why should China see its profitable companies sold for yet more freely-created US dollars, which the central bank must use to buy low-yielding US Treasury bills or lose yet further money on Wall Street?

To avoid this quandary it is necessary to reverse the philosophy of open capital markets that the world has held ever since Bretton Woods in 1944. On the occasion of Mr. Geithner’s visit to China, “Zhou Xiaochuan, minister of the Peoples Bank of China, the country’s central bank, said pointedly that this was the first time since the semiannual talks began in 2006 that China needed to learn from American mistakes as well as its successes” when it came to deregulating capital markets and dismantling controls.8

An era therefore is coming to an end. In the face of continued US overspending, de-dollarization threatens to force countries to return to the kind of dual exchange rates common between World Wars I and II: one exchange rate for commodity trade, another for capital movements and investments, at least from dollar-area economies.

Even without capital controls, the nations meeting at Yekaterinburg are taking steps to avoid being the unwilling recipients of yet more dollars. Seeing that US global hegemony cannot continue without spending power that they themselves supply, governments are attempting to hasten what Chalmers Johnson has called “the sorrows of empire” in his book by that name – the bankruptcy of the US financial-military world order. If China, Russia and their non-aligned allies have their way, the United States will no longer live off the savings of others (in the form of its own recycled dollars) nor have the money for unlimited military expenditures and adventures.

US officials wanted to attend the Yekaterinburg meeting as observers. They were told No. It is a word that Americans will hear much more in the future.

Notes

1 Andrew Scheineson, “The Shanghai Cooperation Organization,” Council on Foreign Relations,

Updated: March 24, 2009: “While some experts say the organization has emerged as a powerful anti-U.S. bulwark in Central Asia, others believe frictions between its two largest members, Russia and China, effectively preclude a strong, unified SCO.”

2 Kremlin.ru, June 5, 2009, in Johnson’s Russia List, June 8, 2009, #8.

3 Jamil Anderlini and Javier Blas, “China reveals big rise in gold reserves,” Financial Times, April 24, 2009. See also “Chinese political advisors propose making yuan an int’l currency.” Beijing, March 7, 2009 (Xinhua). “The key to financial reform is to make the yuan an international currency, said [Peter Kwong Ching] Woo [chairman of the Hong Kong-based Wharf (Holdings) Limited] in a speech to the Second Session of the 11th National Committee of the Chinese People’s Political Consultative Conference (CPPCC), the country’s top political advisory body. That means using the Chinese currency to settle international trade payments …”

4 Shai Oster, “Malaysia, China Consider Ending Trade in Dollars,” Wall Street Journal, June 4, 2009.

5 Jonathan Wheatley, “Brazil and China in plan to axe dollar,” Financial Times, May 19, 2009.

6 “Another Dollar Crisis inevitable unless U.S. starts Saving - China central bank adviser. Global Crisis ‘Inevitable’ Unless U.S. Starts Saving, Yu Says,” Bloomberg News, June 1, 2009. http://www.bloomberg.com/apps/news?pid=20601080&sid=aCV0pFcAFyZw&refer=asia

7 Kathrin Hille, “Lesson in friendship draws blushes,” Financial Times, June 2, 2009.

8 Steven R. Weisman, “U.S. Tells China Subprime Woes Are No Reason to Keep Markets Closed,” The New York Times, June 18, 2008.

‘Perhaps 60% of today’s oil price is pure speculation’ by F. William Engdahl

The price of crude oil today is not made according to any traditional relation of supply to demand. It’s controlled by an elaborate financial market system as well as by the four major Anglo-American oil companies. As much as 60% of today’s crude oil price is pure speculation driven by large trader banks and hedge funds. It has nothing to do with the convenient myths of Peak Oil. It has to do with control of oil and its price. How?

First, the crucial role of the international oil exchanges in London and New York is crucial to the game. Nymex in New York and the ICE Futures in London today control global benchmark oil prices which in turn set most of the freely traded oil cargo. They do so via oil futures contracts on two grades of crude oil—West Texas Intermediate and North Sea Brent.

A third rather new oil exchange, the Dubai Mercantile Exchange (DME), trading Dubai crude, is more or less a daughter of Nymex, with Nymex President, James Newsome, sitting on the board of DME and most key personnel British or American citizens.

Brent is used in spot and long-term contracts to value as much of crude oil produced in global oil markets each day. The Brent price is published by a private oil industry publication, Platt’s. Major oil producers including Russia and Nigeria use Brent as a benchmark for pricing the crude they produce. Brent is a key crude blend for the European market and, to some extent, for Asia.

WTI has historically been more of a US crude oil basket. Not only is it used as the basis for US-traded oil futures, but it's also a key benchmark for US production.

‘The tail that wags the dog’

All this is well and official. But how today’s oil prices are really determined is done by a process so opaque only a handful of major oil trading banks such as Goldman Sachs or Morgan Stanley have any idea who is buying and who selling oil futures or derivative contracts that set physical oil prices in this strange new world of “paper oil.”

With the development of unregulated international derivatives trading in oil futures over the past decade or more, the way has opened for the present speculative bubble in oil prices.

Since the advent of oil futures trading and the two major London and New York oil futures contracts, control of oil prices has left OPEC and gone to Wall Street. It is a classic case of the “tail that wags the dog.”

A June 2006 US Senate Permanent Subcommittee on Investigations report on “The Role of Market Speculation in rising oil and gas prices,” noted, “…there is substantial evidence supporting the conclusion that the large amount of speculation in the current market has significantly increased prices.”

What the Senate committee staff documented in the report was a gaping loophole in US Government regulation of oil derivatives trading so huge a herd of elephants could walk through it. That seems precisely what they have been doing in ramping oil prices through the roof in recent months.

The Senate report was ignored in the media and in the Congress.

The report pointed out that the Commodity Futures Trading Trading Commission, a financial futures regulator, had been mandated by Congress to ensure that prices on the futures market reflect the laws of supply and demand rather than manipulative practices or excessive speculation. The US Commodity Exchange Act (CEA) states, “Excessive speculation in any commodity under contracts of sale of such commodity for future delivery . . . causing sudden or unreasonable fluctuations or unwarranted changes in the price of such commodity, is an undue and unnecessary burden on interstate commerce in such commodity.”

Further, the CEA directs the CFTC to establish such trading limits “as the Commission finds are necessary to diminish, eliminate, or prevent such burden.” Where is the CFTC now that we need such limits?

They seem to have deliberately walked away from their mandated oversight responsibilities in the world’s most important traded commodity, oil.

Enron has the last laugh…

As that US Senate report noted:

“Until recently, US energy futures were traded exclusively on regulated exchanges within the United States, like the NYMEX, which are subject to extensive oversight by the CFTC, including ongoing monitoring to detect and prevent price manipulation or fraud. In recent years, however, there has been a tremendous growth in the trading of contracts that look and are structured just like futures contracts, but which are traded on unregulated OTC electronic markets. Because of their similarity to futures contracts they are often called “futures look-alikes.”

The only practical difference between futures look-alike contracts and futures contracts is that the look-alikes are traded in unregulated markets whereas futures are traded on regulated exchanges. The trading of energy commodities by large firms on OTC electronic exchanges was exempted from CFTC oversight by a provision inserted at the behest of Enron and other large energy traders into the Commodity Futures Modernization Act of 2000 in the waning hours of the 106th Congress.

The impact on market oversight has been substantial. NYMEX traders, for example, are required to keep records of all trades and report large trades to the CFTC. These Large Trader Reports, together with daily trading data providing price and volume information, are the CFTC’s primary tools to gauge the extent of speculation in the markets and to detect, prevent, and prosecute price manipulation. CFTC Chairman Reuben Jeffrey recently stated: “The Commission’s Large Trader information system is one of the cornerstones of our surveillance program and enables detection of concentrated and coordinated positions that might be used by one or more traders to attempt manipulation.”

In contrast to trades conducted on the NYMEX, traders on unregulated OTC electronic exchanges are not required to keep records or file Large Trader Reports with the CFTC, and these trades are exempt from routine CFTC oversight. In contrast to trades conducted on regulated futures exchanges, there is no limit on the number of contracts a speculator may hold on an unregulated OTC electronic exchange, no monitoring of trading by the exchange itself, and no reporting of the amount of outstanding contracts (“open interest”) at the end of each day.” 1

Then, apparently to make sure the way was opened really wide to potential market oil price manipulation, in January 2006, the Bush Administration’s CFTC permitted the Intercontinental Exchange (ICE), the leading operator of electronic energy exchanges, to use its trading terminals in the United States for the trading of US crude oil futures on the ICE futures exchange in London – called “ICE Futures.”

Previously, the ICE Futures exchange in London had traded only in European energy commodities – Brent crude oil and United Kingdom natural gas. As a United Kingdom futures market, the ICE Futures exchange is regulated solely by the UK Financial Services Authority. In 1999, the London exchange obtained the CFTC’s permission to install computer terminals in the United States to permit traders in New York and other US cities to trade European energy commodities through the ICE exchange.

The CFTC opens the door

Then, in January 2006, ICE Futures in London began trading a futures contract for

West Texas Intermediate (WTI) crude oil, a type of crude oil that is produced and delivered in

the United States. ICE Futures also notified the CFTC that it would be permitting traders in the United States to use ICE terminals in the United States to trade its new WTI contract on the ICE Futures London exchange. ICE Futures as well allowed traders in the United States to trade US gasoline and heating oil futures on the ICE Futures exchange in London.

Despite the use by US traders of trading terminals within the United States to trade US oil, gasoline, and heating oil futures contracts, the CFTC has until today refused to assert any jurisdiction over the trading of these contracts.

Persons within the United States seeking to trade key US energy commodities – US crude oil, gasoline, and heating oil futures – are able to avoid all US market oversight or reporting requirements by routing their trades through the ICE Futures exchange in London instead of the NYMEX in New York.

Is that not elegant? The US Government energy futures regulator, CFTC opened the way to the present unregulated and highly opaque oil futures speculation. It may just be coincidence that the present CEO of NYMEX, James Newsome, who also sits on the Dubai Exchange, is a former chairman of the US CFTC. In Washington doors revolve quite smoothly between private and public posts.

A glance at the price for Brent and WTI futures prices since January 2006 indicates the remarkable correlation between skyrocketing oil prices and the unregulated trade in ICE oil futures in US markets. Keep in mind that ICE Futures in London is owned and controlled by a USA company based in Atlanta Georgia.

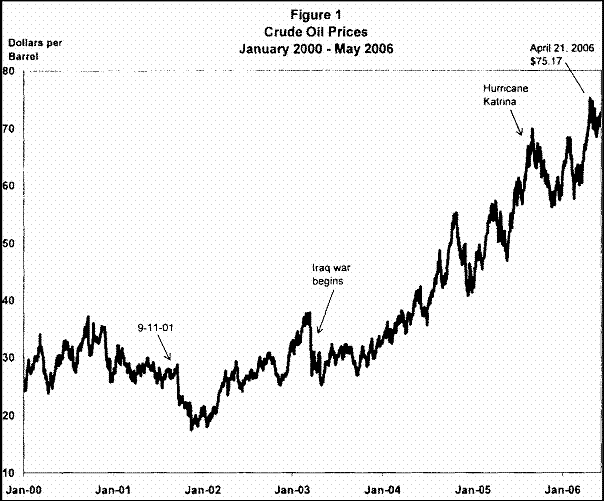

In January 2006 when the CFTC allowed the ICE Futures the gaping exception, oil prices were trading in the range of $59-60 a barrel. Today some two years later we see prices tapping $120 and trend upwards. This is not an OPEC problem, it is a US Government regulatory problem of malign neglect.

By not requiring the ICE to file daily reports of large trades of energy commodities, it is not able to detect and deter price manipulation. As the Senate report noted, “The CFTC's ability to detect and deter energy price manipulation is suffering from critical information gaps, because traders on OTC electronic exchanges and the London ICE Futures are currently exempt from CFTC reporting requirements. Large trader reporting is also essential to analyze the effect of speculation on energy prices.”

The report added, “ICE's filings with the Securities and Exchange Commission and other evidence indicate that its over-the-counter electronic exchange performs a price discovery function -- and thereby affects US energy prices -- in the cash market for the energy commodities traded on that exchange.”

Hedge Funds and Banks driving oil prices

In the most recent sustained run-up in energy prices, large financial institutions, hedge funds, pension funds, and other investors have been pouring billions of dollars into the energy commodities markets to try to take advantage of price changes or hedge against them. Most of this additional investment has not come from producers or consumers of these commodities, but from speculators seeking to take advantage of these price changes. The CFTC defines a speculator as a person who “does not produce or use the commodity, but risks his or her own capital trading futures in that commodity in hopes of making a profit on price changes.”

The large purchases of crude oil futures contracts by speculators have, in effect, created an

additional demand for oil, driving up the price of oil for future delivery in the same manner that additional demand for contracts for the delivery of a physical barrel today drives up the price for oil on the spot market. As far as the market is concerned, the demand for a barrel of oil that results from the purchase of a futures contract by a speculator is just as real as the demand for a barrel that results from the purchase of a futures contract by a refiner or other user of petroleum.

Perhaps 60% of oil prices today pure speculation

Goldman Sachs and Morgan Stanley today are the two leading energy trading firms in the United States. Citigroup and JP Morgan Chase are major players and fund numerous hedge funds as well who speculate.

In June 2006, oil traded in futures markets at some $60 a barrel and the Senate investigation estimated that some $25 of that was due to pure financial speculation. One analyst estimated in August 2005 that US oil inventory levels suggested WTI crude prices should be around $25 a barrel, and not $60.

That would mean today that at least $50 to $60 or more of today’s $115 a barrel price is due to pure hedge fund and financial institution speculation. However, given the unchanged equilibrium in global oil supply and demand over recent months amid the explosive rise in oil futures prices traded on Nymex and ICE exchanges in New York and London it is more likely that as much as 60% of the today oil price is pure speculation. No one knows officially except the tiny handful of energy trading banks in New York and London and they certainly aren’t talking.

By purchasing large numbers of futures contracts, and thereby pushing up futures

prices to even higher levels than current prices, speculators have provided a financial incentive for oil companies to buy even more oil and place it in storage. A refiner will purchase extra oil today, even if it costs $115 per barrel, if the futures price is even higher.

As a result, over the past two years crude oil inventories have been steadily growing, resulting in US crude oil inventories that are now higher than at any time in the previous eight years. The large influx of speculative investment into oil futures has led to a situation where we have both high supplies of crude oil and high crude oil prices.

Compelling evidence also suggests that the oft-cited geopolitical, economic, and natural factors do not explain the recent rise in energy prices can be seen in the actual data on crude oil supply and demand. Although demand has significantly increased over the past few years, so have supplies.

Over the past couple of years global crude oil production has increased along with the increases in demand; in fact, during this period global supplies have exceeded demand, according to the US Department of Energy. The US Department of Energy’s Energy Information Administration (EIA) recently forecast that in the next few years global surplus production capacity will continue to grow to between 3 and 5 million barrels per day by 2010, thereby “substantially thickening the surplus capacity cushion.”

Dollar and oil link

A common speculation strategy amid a declining USA economy and a falling US dollar is for speculators and ordinary investment funds desperate for more profitable investments amid the US securitization disaster, to take futures positions selling the dollar “short” and oil “long.”

For huge US or EU pension funds or banks desperate to get profits following the collapse in earnings since August 2007 and the US real estate crisis, oil is one of the best ways to get huge speculative gains. The backdrop that supports the current oil price bubble is continued unrest in the Middle East, in Sudan, in Venezuela and Pakistan and firm oil demand in China and most of the world outside the US. Speculators trade on rumor, not fact.

In turn, once major oil companies and refiners in North America and EU countries begin to hoard oil, supplies appear even tighter lending background support to present prices.

Because the over-the-counter (OTC) and London ICE Futures energy markets are unregulated, there are no precise or reliable figures as to the total dollar value of recent spending on investments in energy commodities, but the estimates are consistently in the range of tens of billions of dollars.

The increased speculative interest in commodities is also seen in the increasing popularity of commodity index funds, which are funds whose price is tied to the price of a basket of various commodity futures. Goldman Sachs estimates that pension funds and mutual funds have invested a total of approximately $85 billion in commodity index funds, and that investments in its own index, the Goldman Sachs Commodity Index (GSCI), has tripled over the past few years. Notable is the fact that the US Treasury Secretary, Henry Paulson, is former Chairman of Goldman Sachs.

F. William Engdahl is an Associate of the Centre for Research on Globalization (CRG) and author of A Century of War: Anglo-American Oil Politics and the New World Order. He may be contacted at info@engdahl.oilgeopolitics.net

1 United States Senate Premanent Subcommittee on Investigations, 109th Congress 2nd Session, The Role of Market speculation in Rising Oil and Gas Prices: A Need to Put the Cop Back on the Beat; Staff Report, prepared by the Permanent Subcommittee on Investigations of the Committee on Homeland Security and Governmental Affairs, United States Senate, Washington D.C., June 27, 2006. p. 3.

BUT ...

"Now, speculators do sometimes push commodity prices far above the level justified by fundamentals. But when that happens, there are telltale signs that just aren’t there in today’s oil market.

Imagine what would happen if the oil market were humming along, with supply and demand balanced at a price of $25 a barrel, and a bunch of speculators came in and drove the price up to $100.

Even if this were purely a financial play on the part of the speculators, it would have major consequences in the material world. Faced with higher prices, drivers would cut back on their driving; homeowners would turn down their thermostats; owners of marginal oil wells would put them back into production.

As a result, the initial balance between supply and demand would be broken, replaced with a situation in which supply exceeded demand. This excess supply would, in turn, drive prices back down again — unless someone were willing to buy up the excess and take it off the market.

The only way speculation can have a persistent effect on oil prices, then, is if it leads to physical hoarding — an increase in private inventories of black gunk. This actually happened in the late 1970s, when the effects of disrupted Iranian supply were amplified by widespread panic stockpiling.

But it hasn’t happened this time: all through the period of the alleged bubble, inventories have remained at more or less normal levels. This tells us that the rise in oil prices isn’t the result of runaway speculation; it’s the result of fundamental factors, mainly the growing difficulty of finding oil and the rapid growth of emerging economies like China. The rise in oil prices these past few years had to happen to keep demand growth from exceeding supply growth."

I think the contango situation this year did have the effect of pulling some oil temporarily off the market, but that was for a short time period and in rather unusual circumstances: seekingalpha.com/user/...

Those circumstances did not exist in the summer of 2008 when prices were spiking, and I don't believe hoarding was the cause of that spike. If we look at the Energy Information Administration numbers for 2008 (1), in fact, we see that consumption exceeded production for the 1st half of the year, before it dropped in the second half. Consumption and production were roughly in balance for the year.

Total World Production ..................... 85.72 (1st Q) 85.70 (2nd Q) 85.43 (3rd Q) 85.10 (4th Q) = 85.49 (2008 avg.)

Total World Consumption ................. 86.52 (1st Q) 86.07 (2nd Q) 85.10 (3rd Q) 84.07 (4th Q) = 85.43 (2008 avg.)

In other words we had a worldwide stock draw from inventories of .80 million barrels per day in the 1st Q of 2008, & .36 mbd in the 2nd quarter. It wasn't until we went into a worldwide recession and demand dropped by more than 1 mbd in the 3rd quarter and almost another mbd in the 4th that we had a small surplus build.

From your link:

"In January 2006 when the CFTC allowed the ICE Futures the gaping exception, oil prices were trading in the range of $59-60 a barrel. Today some two years later we see prices tapping $120 and trend upwards. This is not an OPEC problem, it is a US Government regulatory problem of malign neglect."

I used a similar argument in an unsuccessful attempt at humor in a high school homework assignment. I noted in the paper the amazing correlation between the growth in students taking english classes in the 20th century and the number of people committed to mental institutions, concluding, of course, that english classes caused mental illness. My english teacher didn't think it was too funny and gave me a "D" for committing the "Post-hoc ergo propter hoc" logical fallacy, aka "confusing association with causation".

But the bottom line for me, once again, is that I remain unconvinced by that article that in May 2008 "Perhaps 60% of today’s oil price is pure speculation". I would be looking for evidence that the "speculators" were bidding the prices up higher than would be explainable by supply and demand, telltale signs of which would be a growing buildup in inventories as Mr. Krugman noted. But from what I can tell, that was not the case.

As it stands, I'm more inclined at the moment to believe something close to the opinion expressed in an editorial in Energy Current:

"After many years of solid growth, oil production plateaued in October 2004. Regardless of the price level, the oil supply simply stopped responding, and from then on, the world had to make do with broadly flat supplies. ... demand accommodation was required. This was achieved by secular prices rises averaging 25 percent per annum from 2003 to the end of 2007. In other words, the price of oil went up, and this constrained consumption by causing the marginal consumer to drop out of the market. ...by the second half 2007, the situation was becoming critical. Consumption was being maintained by continuing draws on inventories averaging 1.4 mbpd, and virtually every producer, with the possible exception of the Saudis, was running flat out. By early 2008, even the Saudis were throwing the kitchen sink at the market - all to no avail. On paper, it looked like a peak oil nightmare.

Of course, consumers were responding. From 2005, the EU and Japan began to shed consumption and, from late 2007, US consumption also began to decline as the US consumer sought to escape high oil prices. Notwithstanding, developed economy consumers were not abandoning the market as fast as Chinese consumers were entering it, and prices continued to rise. In early 2008, prices took off and some argue that speculation took over. Still, as inventories continued to fall until May 2008 and all the oil producers were running at full output, the case for market manipulation at that time is hard to make. Indeed, the market was in backwardation most of this time. In backwardation, futures prices are lower than spot prices, the equivalent of the market saying, "Well, prices are high now, but they'll be lower later." The market - those very speculators - believed that oil was over-priced but was continually surprised as demand kept pushing up prices." (2)

Endnotes:

1. International Crude Oil and Liquid Fuels Supply, Consumption, and Inventories (2008, 2009 & 2010 projections as of June 2009)

www.eia.doe.gov/emeu/s...

2. EDITORIAL: Peak oil, not speculation; 5/11/2009; by Steven Kopits, Managing Director, Douglas-Westwood, New York

www.energycurrent.com/...

Thursday, June 25, 2009

AIG committed 10(b) 5 fraud by misrepresenting material company conditions

Recently uncovered critical documents disclosing details about AIG's CDO portfolio and collateral calls, indicate that during a December 5th conference call with Investors, Joe Cassano, famous for singlehandedly destroying capitalism and forcing most financial companies to be subsidized by US taxpayers in perpetuity, as well as then CEO Martin Sullivan, effectively committed 10(b) 5 fraud by misrepresenting material company conditions.

The collateral disclosure, courtesy of CBS News, which comes from an email sent by Joseph Cassano to Bill Dooley on November 27, a week before the fateful "all is good" conference call, identifies $66.7 Billion in CDO Negative basis trades with 9 counterparties, most of which demand collateral to cover mark discrepancies amounting to a total of just over $4 billion. Not surprisingly, Goldman dominates the list in terms of both CDO exposure and collateral demands, with $23 billion of negative basis CDOs which according to Goldman resulting a collateral post of $3 billion.

hat tip Thomas

The full email support indicating Cassano's and Dooley's knowledge of just how underwater the firm was in the last week of November, is presented below (also available here and here).

What supports a case of 10(b) 5 violation are some of the exchanges in the ensuing December 5th, 2007 conference call (posted below in its entirety).

Probably one of the most notable utterances is that of Joseph Cassano himself, who somehow is still not facing major criminal securities fraud charges against him:

And we have from time to time gotten collateral calls from people and then we say to them, well we don't agree with your numbers. And they go, oh, and they go away. And you say well what was that? It's like a drive by in a way. And the other times they sat down with us, and none of this is hostile or anything, it's all very cordial, and we sit down and we try and find the middle ground and compare where we are. And that goes to some of this price discovery I've been talking about and how we go through that price discovery process.Probably an even bigger smoking gun is this phrase by CEO Martin Sullivan, who, obviously had received all his substantiating data from none other than Joe Cassano.

[B]ecause this business is carefully underwritten and structured with very high attachment points to the multiples of expected losses, we believe the probability that it will sustain an economic loss is close to zero.

Did Sullivan and Joseph not have a regulatory obligation to disclose just how dire the economic loss potential on their "business" was simply as a result of the major CDO collateral calls (which they blew off as friendly banter)? Only the SEC knows the answer (and will likely take it to its grave).

Lastly, and maybe even more relevantly, is the question of the major discrepancies in disputed CDO marks between most counterparties and those of Goldman Sachs and SocGen. And while the SocGen collateral post demand has not been made clear in the email, that of Goldman, with their aggressively priced CDOs, results in a collateral call of nearly 13% ($3 billion) of GS's total negative basis exposure of $23 billion: more than double that of next closest disclosed counterparty Calyon which was at a total 7.6% collateral demand. What brought about this aggressive book mark down by GS? Also, did SocGen's Jerome Kerviel futures implosion in January 2008 have anything to do with the pain the firm was obviously experiencing as a result of book losses on its AIG CDOs? Did these actions have anything to do with the fact that the more substantial the write down, the greater the subsequent payoff to the firm (once the system became unravelled and taxpayers ended up paying Goldman and others for their collateral demands). Of course, the real question here, as everywhere else, is how much did Goldman do to precipitate the collapse: both of Bear, of Lehman, and of AIG.

This is an answer that only Cassano potentially would be able to shed some light on - is it not about time to have Joseph respond to a myriad of pent up questions about not only his potentially illegal conference call disclosures but also his conversations with major AIG counterparties such as Goldman Sachs?

Subscribe to:

Posts (Atom)